Set your financial goals

A well-thought-out approach to managing your money can better prepare you to handle different needs and changes in your life. You can begin by identifying your short and long-term needs, and how to go about meeting them.

Develop a saving habit early with retirement in mind. To see tangible increases in your savings account, set aside 15-20% of your salary each month as a start. Draw up a budget and make a plan for your savings and investments to help meet your financial goals.

Your CPF accounts

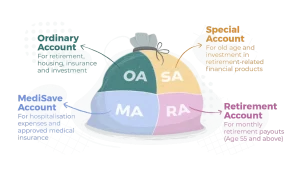

The Central Provident Fund (CPF) is a comprehensive social security savings plan, which helps meet your retirement, housing and healthcare needs. Each month, you and your employer contribute to your CPF, which consists of three different accounts: Ordinary, Special and MediSave.

Through schemes such as Workfare and MediSave top-ups for senior citizens, the government also helps to supplement the CPF savings of lower-wage workers.

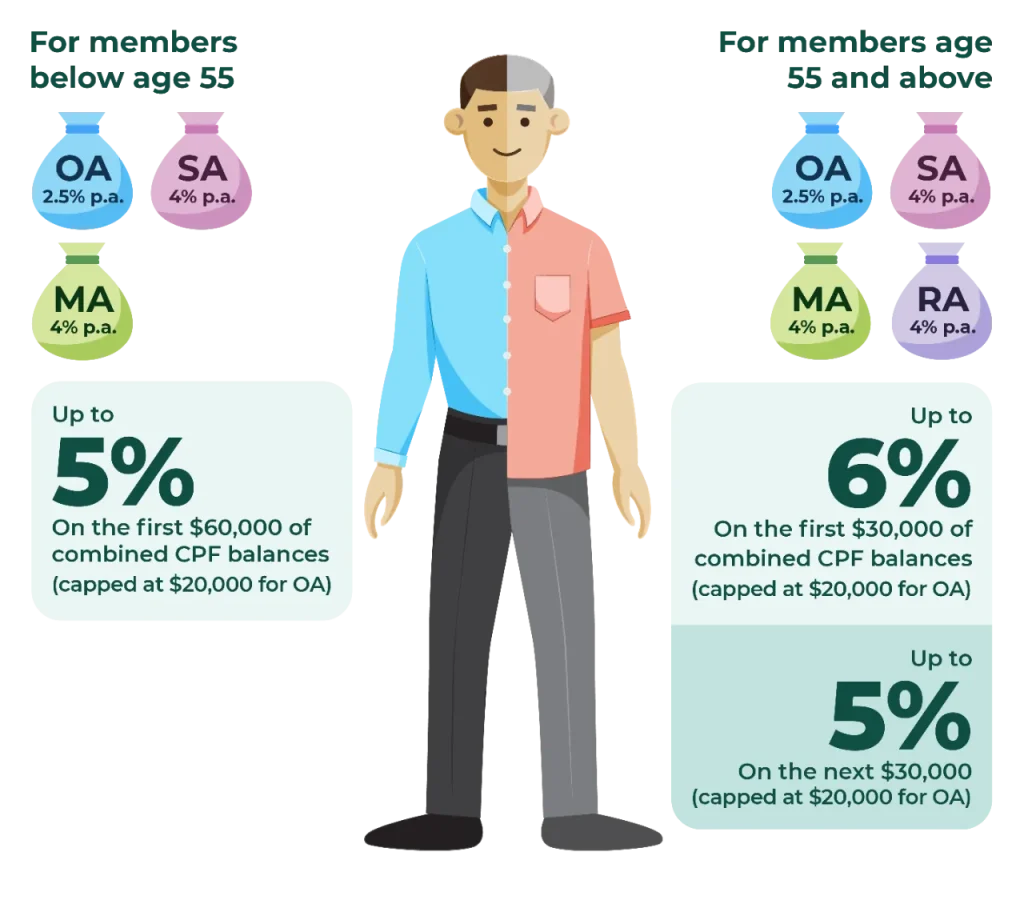

Here’s a summary of the interest rates and uses for each account:

As a new entrant to the workforce, your contributions to your CPF accounts each month totals 37%, with 20% coming from your salary and 17% coming from your employer*. Do note that if you are a Singapore Permanent Resident, your contributions will start at a lower rate and grow to 37% after two years.

*Based on CPF contribution rate for employees 55 years old and below (for monthly salary more than or equivalent to $750). CPF contributions are payable for your monthly salary of up to $6,000.

Find out more about CPF contribution and allocation rates.

Know your employment rights

If you work in Singapore, you are entitled to employment rights, which include minimum terms and conditions of employment, as well as the rights and responsibilities of employees and employers under a contract of service. This extends to mandatory CPF contributions by your employer, as long as you earn more than $50 a month.

Find out more about your employment rights.

Dependants’ Protection Scheme

It is always good to be prepared for the unexpected.

If you are at least 21 years old and have made your first CPF contribution, you will automatically be covered under the Dependants’ Protection Scheme, an affordable term insurance that covers insured members up to 65 years. Members up to 60 years old will be covered for a maximum of $70,000 while those above 60 to 65 are covered for a maximum of $55,000. The Dependants’ Protection Scheme benefit will be paid out to you and/your family members should you become permanently unfit for work or pass away. You can use the monies from your Ordinary and/or Special Account or cash to pay for the annual premiums.

Education loan

Your education loan is likely to be one of your first financial obligations. Just like any other loan, if you had used CPF savings for your education, you would need to repay the amount (including interest accrued) to the CPF account you used.

Repayment of the education loan begins one year after graduation or the termination of studies, whichever is earlier. About three months before the start of the repayment, you will receive a package with the loan repayment details. You can begin repaying your loan earlier if you have additional cash in hand.

Find out more about the CPF Education Loan Scheme.

Investments

Having just entered the workforce, you may be keen to make investments and grow your savings as part of your financial plan. Remember that all investments come with risks, so it is good to be familiar with investment concepts and products before embarking on any investment plans. Learn more about basic investing concepts here before you start investing.

The CPF Investment Scheme allows you to invest with your CPF savings through various investment products. To make an investment using your CPF savings, you should:

- Be at least 18 years old;

- Not be an undischarged bankrupt; and

- Have more than $20,000 in your Ordinary Account and/or more than $40,000 in your Special Account

Find out more about CPF and Investing.

Growing your savings

To help you grow your CPF savings and earn attractive risk-free interest rates, you can consider making top-ups beyond the mandatory CPF contributions. This can be through the CPF Retirement Sum Topping-Up Scheme and by making CPF voluntary contributions.

The Retirement Sum Topping-Up Scheme allows you to

- Top up with cash or transfer your CPF savings

- Top up your own or your loved ones’* Special Accounts (below age 55) or Retirement Accounts (age 55 and above)

Topping up with cash or a CPF transfer to the Full Retirement Sum (below age 55) or Enhanced Retirement Sum (age 55 and above) gives the opportunity to enjoy a higher monthly payout for life. You can enjoy tax relief of up to $16,000 per year if you use cash to top up for yourself (up to $8,000) and your loved ones (up to $8,000).

You can also make voluntary contributions, through a lump sum payment or GIRO, to build up you and/or your loved ones’ CPF savings. Voluntary contributions to all your CPF accounts (Ordinary, Special and MediSave Accounts) are subject to the approved limit and do not qualify for tax deduction. However, voluntary contributions to your MediSave Account alone are tax deductible.

For more information on making voluntary contributions.

*”Loved ones” include only your parents, parents-in-law, grandparents, grandparents-in-law, spouse and siblings.

Supplementary Retirement Scheme

The Supplementary Retirement Scheme is a voluntary scheme that allows you to save for retirement, complementing your CPF savings. Both you and your employer can participate in this scheme and enjoy tax reliefs. Find out more.

Making financial plans and saving early means you’re ready to face the different needs that may arise in the future. Even as you embark on your first job, you can begin to grow your savings to secure your nest egg by leveraging on the various schemes available.

This article is contributed by CPF Board.

![]()